Current Mortgage Rates 2026: Refinancing & New Home Purchase Analysis

Current Mortgage Rates in 2026: A Comparative Analysis for Refinancing Opportunities and New Home Purchases

Navigating the housing market requires a keen understanding of various economic indicators, with mortgage rates 2026 standing out as a pivotal factor. As we delve deeper into 2026, both prospective homebuyers and current homeowners considering refinancing are keenly observing the trends, forecasts, and underlying economic forces shaping these rates. The landscape of mortgage financing is ever-evolving, influenced by global economics, domestic policies, and market sentiment.

This comprehensive analysis aims to shed light on the current state of mortgage rates 2026, offering a comparative perspective for those looking to purchase a new home or optimize their existing mortgage through refinancing. We’ll explore the key drivers behind these rates, examine expert predictions, and provide actionable insights to help you make informed financial decisions in this dynamic environment. Understanding the nuances of the market today can significantly impact your financial future, whether you’re securing your first home or enhancing your long-term investment strategy.

Understanding the Economic Landscape Influencing Mortgage Rates 2026

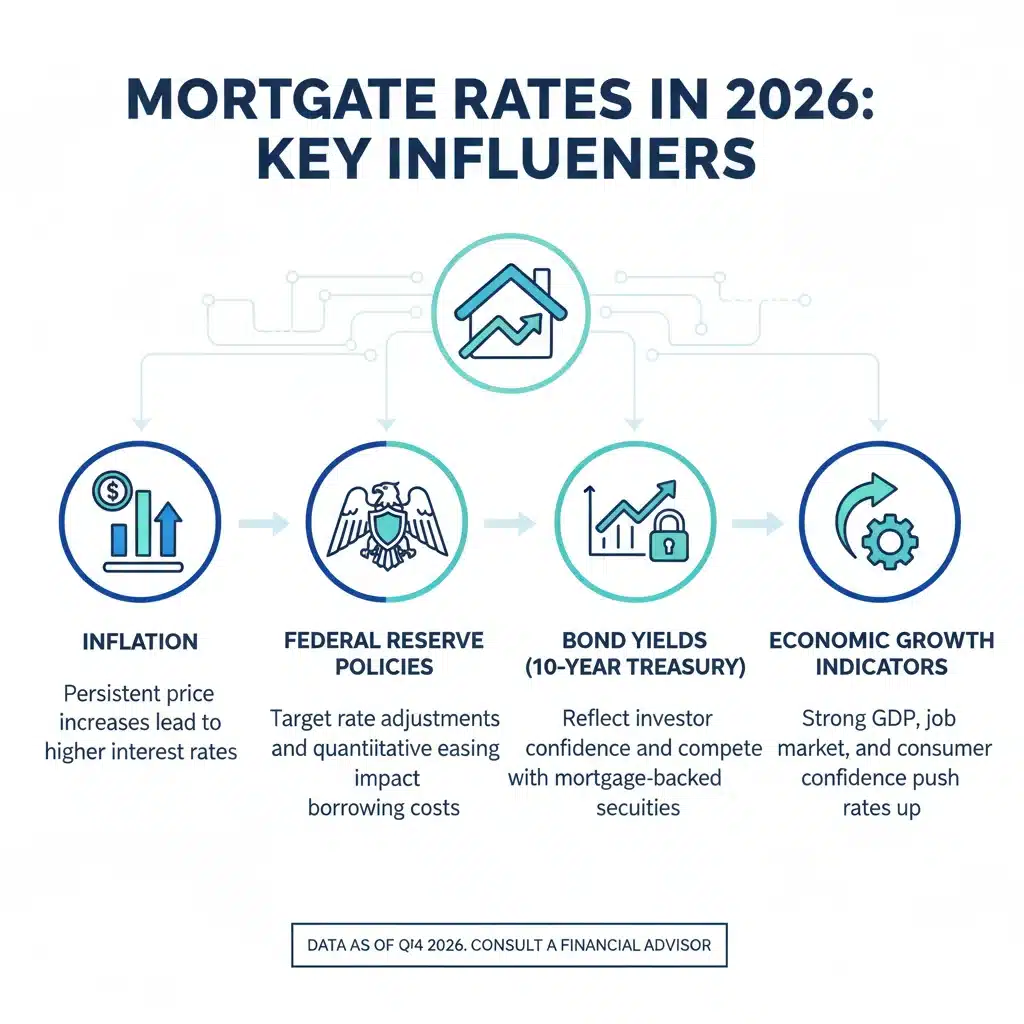

The trajectory of mortgage rates 2026 is not an isolated phenomenon; it’s intricately linked to a broader economic narrative. Several macroscopic factors exert significant influence, creating a complex interplay that determines the cost of borrowing for home loans. To truly grasp where rates are headed, it’s essential to dissect these foundational elements.

Inflation and Monetary Policy

Inflation remains a primary driver. When inflation is high, central banks, like the Federal Reserve in the United States, typically respond by raising the federal funds rate. While this isn’t directly the mortgage rate, it influences the cost of borrowing for banks, which in turn affects the rates they offer consumers. Conversely, a stable or declining inflationary environment might give central banks room to ease monetary policy, potentially leading to lower mortgage rates. In 2026, the ongoing battle against inflation, coupled with efforts to maintain economic stability, will be a critical determinant.

Federal Reserve Actions and Bond Yields

The Federal Reserve’s actions, particularly its decisions on interest rates and its balance sheet policies (quantitative easing or tightening), have a profound impact. Mortgage rates are closely tied to the yield on the 10-year Treasury bond. When the Fed signals a more hawkish stance, bond yields tend to rise, pulling mortgage rates upward. A dovish stance, on the other hand, can lead to lower yields and, consequently, lower mortgage rates. Market participants will be scrutinizing every Fed announcement and economic projection throughout 2026 for clues regarding future rate movements.

Economic Growth and Employment Data

A robust economy, characterized by strong GDP growth and low unemployment, often correlates with higher inflation and, subsequently, higher interest rates. Lenders perceive a strong economy as an environment where borrowers are more likely to repay their loans, but the increased demand for credit can also push rates up. Conversely, signs of economic slowdown or recession can lead to lower rates as investors seek the safety of bonds, driving down yields. Employment reports, consumer confidence indices, and manufacturing data will provide vital insights into the overall health of the economy and its potential impact on mortgage rates 2026.

Global Economic Factors

The interconnectedness of the global economy means that international events can also ripple through to domestic mortgage markets. Geopolitical stability, global trade relations, and economic performance in major world economies can all influence investor sentiment and capital flows, impacting bond yields and, by extension, mortgage rates. While often less direct than domestic factors, global dynamics should not be overlooked when assessing the outlook for mortgage rates 2026.

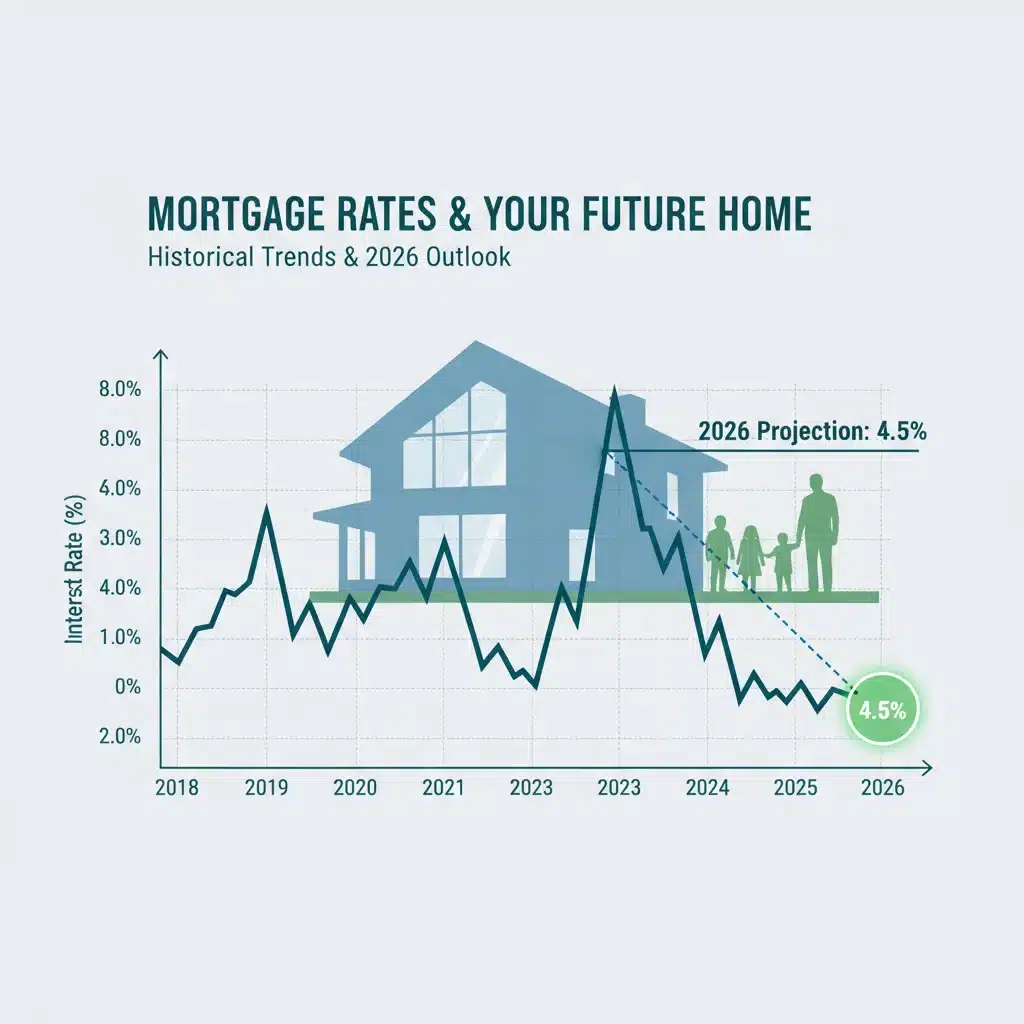

Current Mortgage Rates 2026: A Snapshot

As we navigate through 2026, the mortgage market presents a nuanced picture. While specific rates fluctuate daily and depend on individual borrower profiles, we can identify general trends and ranges for common mortgage products. It’s crucial to remember that these are averages, and your specific rate will be influenced by your credit score, loan-to-value ratio, loan type, and lender.

30-Year Fixed-Rate Mortgages (FRM)

The 30-year fixed-rate mortgage remains the most popular choice for homebuyers due to its predictable monthly payments. In 2026, these rates have shown a degree of volatility, reflecting the ongoing economic adjustments. Early 2026 saw rates stabilize somewhat after the fluctuations of previous years, but minor upward or downward pressures continue to assert themselves based on incoming economic data. The average 30-year FRM is generally hovering within a range that makes homeownership accessible, though perhaps less historically affordable than during periods of exceptionally low rates.

15-Year Fixed-Rate Mortgages (FRM)

For those who can afford higher monthly payments, the 15-year fixed-rate mortgage offers significant savings on interest over the life of the loan. These rates are typically lower than their 30-year counterparts. In 2026, the spread between 15-year and 30-year rates continues to provide an attractive option for borrowers aiming to pay off their homes sooner and with less overall cost. The stability of fixed rates, regardless of the term, offers peace of mind against future rate hikes.

Adjustable-Rate Mortgages (ARM)

Adjustable-rate mortgages (ARMs) have gained renewed attention in environments where fixed rates are perceived as high. These loans typically offer a lower initial interest rate for a fixed period (e.g., 5/1, 7/1, or 10/1 ARM), after which the rate adjusts periodically based on a predetermined index. In 2026, ARMs can be an attractive option for borrowers who anticipate selling or refinancing before the adjustment period, or for those who believe rates will decline in the future. However, they come with the inherent risk of payment increases if rates rise significantly. Understanding the caps and adjustment frequency is paramount when considering an ARM.

Jumbo Loan Rates

For mortgages exceeding the conforming loan limits set by Fannie Mae and Freddie Mac, jumbo loan rates apply. These rates can sometimes be slightly higher or lower than conforming rates, depending on the lender and market conditions. In 2026, the jumbo loan market reflects the overall health of the luxury housing sector and the risk appetite of lenders. Borrowers seeking jumbo loans typically require excellent credit and significant down payments.

Refinancing Opportunities in 2026

For current homeowners, the question of whether to refinance is a perennial one, and mortgage rates 2026 play a central role in this decision. Refinancing can offer several benefits, from lowering monthly payments to shortening loan terms or tapping into home equity. However, it’s not a one-size-fits-all solution, and careful consideration is required.

When Does Refinancing Make Sense?

- Lowering Your Interest Rate: The most common reason to refinance is to secure a lower interest rate than your current mortgage. Even a small reduction can lead to substantial savings over the life of the loan. In 2026, if rates have fallen since you originated your mortgage, or if your credit score has significantly improved, refinancing could be highly beneficial.

- Reducing Monthly Payments: By securing a lower rate or extending your loan term (e.g., from a 15-year to a 30-year mortgage), you can reduce your monthly housing expenses, freeing up cash flow for other financial goals.

- Shortening Your Loan Term: Conversely, if current mortgage rates 2026 are favorable, you might consider refinancing from a 30-year to a 15-year mortgage. While this increases your monthly payment, it drastically reduces the total interest paid and allows you to build equity faster.

- Cash-Out Refinance: This option allows you to tap into your home equity by taking out a new, larger mortgage and receiving the difference in cash. This cash can be used for home improvements, debt consolidation, or other significant expenses. However, it’s crucial to use this option responsibly, as you’re essentially converting home equity into debt.

- Switching from an ARM to a Fixed-Rate Mortgage: If you have an adjustable-rate mortgage and anticipate future rate increases, refinancing into a fixed-rate mortgage can provide stability and protection against payment shock.

Costs Associated with Refinancing

It’s important to factor in the closing costs associated with refinancing, which can typically range from 2% to 5% of the loan amount. These costs include appraisal fees, title insurance, origination fees, and other administrative charges. You’ll need to calculate whether the savings from a lower interest rate or other benefits outweigh these upfront costs. A break-even analysis can help determine how long it will take to recoup the refinancing expenses.

New Home Purchases in the 2026 Market

For aspiring homeowners, navigating the 2026 housing market involves understanding not just mortgage rates 2026 but also home prices, inventory levels, and overall market competition. Each of these elements contributes to the affordability and feasibility of purchasing a new home.

Affordability and Home Prices

Home prices have seen significant appreciation in recent years, making affordability a key concern for many buyers. While some markets may experience stabilization or even slight corrections in 2026, overall demand often outstrips supply in desirable areas. Your ability to afford a home will largely depend on your income, savings for a down payment, and the prevailing mortgage rates 2026. A higher interest rate means a higher monthly payment for the same loan amount, reducing your purchasing power.

Inventory Levels and Competition

Inventory levels continue to be a critical factor. Low housing inventory can lead to bidding wars and homes selling above asking price, even in a higher interest rate environment. In 2026, while new construction may alleviate some supply constraints, many markets still face an imbalance. Buyers need to be prepared for potentially competitive situations and act quickly when suitable properties become available.

Pre-Approval and Financial Preparedness

Securing mortgage pre-approval is more crucial than ever in 2026. A pre-approval letter from a lender demonstrates your seriousness as a buyer and gives you a clear understanding of how much you can afford. It also allows you to lock in a rate for a certain period, protecting you from potential rate increases while you search for a home. Beyond pre-approval, ensuring a strong credit score, a stable income, and sufficient savings for a down payment and closing costs will significantly strengthen your position.

Expert Predictions and Outlook for Mortgage Rates 2026

Predicting the future of mortgage rates 2026 with absolute certainty is challenging, given the multitude of variables at play. However, various financial institutions and economic analysts offer projections based on their assessments of the global and domestic economic outlook.

Consensus on Gradual Stabilization

Many experts anticipate a period of gradual stabilization for mortgage rates 2026, following the significant shifts observed in previous years. This doesn’t necessarily mean rates will remain static, but rather that extreme volatility might lessen. The consensus often points to rates remaining within a range that reflects moderate inflation and a Federal Reserve that is balancing economic growth with price stability.

Potential for Slight Fluctuations

While stabilization is a general outlook, slight fluctuations are always possible. Unexpected geopolitical events, stronger-than-anticipated economic data, or a resurgence of inflationary pressures could push rates higher. Conversely, signs of economic slowdown or a successful taming of inflation could lead to modest declines. Borrowers should remain agile and monitor economic news closely.

Long-Term Outlook

In the longer term, beyond 2026, the trajectory of mortgage rates will largely depend on structural economic changes, demographic shifts, and technological advancements. However, for the immediate future, the focus remains on the interplay of inflation, central bank policy, and overall economic health. It’s important to consult with financial advisors and mortgage professionals who can provide personalized insights based on the most current data.

Strategies for Navigating Mortgage Rates 2026

Whether you’re looking to buy a home or refinance, having a strategic approach is essential in the current interest rate environment. Here are some actionable tips to help you make the best financial decisions regarding mortgage rates 2026.

For Homebuyers:

- Get Pre-Approved: As mentioned, this is non-negotiable. It clarifies your budget, streamlines the offer process, and often allows you to lock in a rate.

- Improve Your Credit Score: A higher credit score can qualify you for the best possible interest rates. Pay bills on time, reduce credit card debt, and avoid opening new lines of credit before applying for a mortgage.

- Save for a Larger Down Payment: A larger down payment reduces the loan amount, lowers your monthly payments, and can help you avoid private mortgage insurance (PMI). It also signals less risk to lenders, potentially securing you a better rate.

- Shop Around for Lenders: Don’t settle for the first offer. Compare rates and terms from multiple lenders, including banks, credit unions, and online mortgage brokers. Even a small difference in interest rate can save you tens of thousands over the life of the loan.

- Consider an ARM Strategically: If you plan to move or refinance within the initial fixed-rate period, an ARM might offer a lower starting rate. Just be fully aware of the adjustment terms and your risk tolerance.

For Homeowners Considering Refinancing:

- Monitor Current Rates: Keep an eye on mortgage rates 2026. If they drop significantly below your current rate, it’s a good time to explore refinancing.

- Calculate Your Break-Even Point: Determine how long it will take for the savings from a lower interest rate to offset the refinancing closing costs. If you plan to move before reaching this point, refinancing might not be worthwhile.

- Assess Your Financial Goals: Are you looking to lower payments, shorten your term, or access cash? Your primary goal will dictate the best refinancing product for you.

- Review Your Credit and Equity: A strong credit score and substantial home equity will provide you with more favorable refinancing options.

- Consult with a Mortgage Professional: An experienced loan officer can help you evaluate your options, understand the costs, and determine if refinancing aligns with your financial objectives.

The Role of Technology in Mortgage Applications

In 2026, technology continues to transform the mortgage application process, making it more efficient and transparent. Online applications, digital document submission, and AI-powered underwriting are becoming standard. This digital evolution can speed up the approval process and, in some cases, lead to more competitive rates due to reduced operational costs for lenders. Borrowers can leverage these tools to compare offers quickly and manage their applications more effectively.

Furthermore, financial technology (FinTech) platforms are providing sophisticated analytics that help consumers understand how various economic factors might influence mortgage rates 2026. These platforms often offer calculators and simulators that allow users to model different scenarios, helping them to visualize the impact of interest rate changes on their monthly payments and overall loan cost. Staying abreast of these technological advancements can empower you to make more informed decisions.

Understanding Different Mortgage Products in Detail

Beyond the basic 30-year fixed and 15-year fixed options, the mortgage market in 2026 offers a variety of specialized products that might be suitable for specific borrower needs. A deeper dive into these can reveal opportunities you might not have considered.

FHA Loans

FHA loans, insured by the Federal Housing Administration, are popular among first-time homebuyers or those with lower credit scores and smaller down payments. In 2026, FHA loans continue to offer competitive rates and more lenient qualification criteria compared to conventional loans. However, they typically require mortgage insurance premiums (MIP) for the life of the loan, which adds to the overall cost. Understanding the specific FHA guidelines for 2026 is crucial if this is your chosen path.

VA Loans

For eligible service members, veterans, and their spouses, VA loans offer significant benefits, including no down payment requirements and no private mortgage insurance. These government-backed loans often come with some of the most favorable mortgage rates 2026. If you qualify, a VA loan can be an incredibly powerful tool for homeownership, reducing upfront costs and long-term expenses. The eligibility criteria and funding fee structure should be thoroughly reviewed.

USDA Loans

Designed for low-to-moderate income borrowers in eligible rural and suburban areas, USDA loans also offer no down payment options. These loans are backed by the U.S. Department of Agriculture and aim to promote homeownership in less dense regions. While specific income and property location restrictions apply, USDA loans can provide an excellent pathway to homeownership for qualified individuals in 2026, often with highly competitive interest rates and reduced mortgage insurance compared to FHA loans.

Interest-Only Mortgages and Other Niche Products

While less common for primary residences, some niche products like interest-only mortgages exist. These allow borrowers to pay only the interest for a set period, resulting in lower initial monthly payments. However, the principal balance does not decrease during this time, and payments can jump significantly once the interest-only period ends. These are typically considered by sophisticated investors or those with fluctuating incomes. Due diligence is paramount when exploring such specialized options, especially given the current economic climate and mortgage rates 2026.

The Impact of Global Events on Mortgage Rates

The world is more interconnected than ever, and major global events can send ripples through financial markets, ultimately affecting mortgage rates 2026. While domestic economic policy and inflation are often the most direct drivers, broader international developments cannot be ignored.

Geopolitical Stability

Periods of geopolitical instability often lead to a ‘flight to safety’ among investors, who tend to move their capital into traditionally safe assets like U.S. Treasury bonds. This increased demand for bonds can drive down their yields, which in turn can push mortgage rates lower. Conversely, a stable global environment might see investors seeking higher returns elsewhere, potentially leading to higher bond yields and mortgage rates.

Global Economic Performance

The economic health of major global players – think China, the Eurozone, and Japan – can indirectly influence the U.S. economy and, by extension, its interest rates. A global economic slowdown, for instance, might prompt central banks worldwide to adopt more accommodative monetary policies, which could contribute to lower rates globally, including for U.S. mortgages.

Supply Chain Disruptions and Commodity Prices

Ongoing supply chain issues and fluctuations in global commodity prices (especially oil) can fuel inflationary pressures. If these pressures persist globally, they can prompt central banks to maintain or even increase interest rates to curb inflation, impacting mortgage rates 2026. Monitoring these international economic indicators provides a more holistic view of potential rate movements.

Making an Informed Decision in 2026

The decision to buy a home or refinance an existing mortgage is one of the most significant financial choices many individuals and families will make. In 2026, with the dynamic nature of mortgage rates 2026 and the broader economic environment, making an informed decision is more important than ever.

It requires a combination of self-assessment, market research, and expert consultation. Understand your financial health, including your credit score, debt-to-income ratio, and available savings. Research not just interest rates but also local housing market conditions, including inventory, home price trends, and future development plans. Finally, engage with reputable mortgage professionals who can offer tailored advice and help you navigate the complexities of loan products and application processes.

By taking a proactive and well-researched approach, you can position yourself to leverage the opportunities presented by the 2026 mortgage market, whether you’re securing your dream home or optimizing your current financial situation. Remember, the goal is not just to find the lowest rate, but the best overall mortgage solution that aligns with your long-term financial goals and risk tolerance.

Final Thoughts on Mortgage Rates 2026

The landscape of mortgage rates 2026 is characterized by continued responsiveness to inflation, central bank policy, and broader economic indicators. While volatility may be less pronounced than in previous years, an informed approach is still critical. For prospective homebuyers, careful financial planning, strong credit, and diligent market research will be your greatest allies. For homeowners, consistently evaluating your current mortgage against prevailing rates can unlock significant savings or provide much-needed financial flexibility.

Ultimately, staying educated on market trends, understanding the economic forces at play, and seeking professional guidance are the best ways to navigate the complexities of the 2026 mortgage market. Your financial well-being hinges on making strategic choices, and with the right information, you can confidently move forward in your homeownership journey.