HSA Maximization 2026: New Limits & Tax Advantages for US Families

Maximizing your Health Savings Account (HSA) in 2026 is crucial for U.S. families seeking to leverage new contribution limits, significant tax advantages, and strategic planning to enhance both health and financial security.

Are you ready to optimize your healthcare savings and build a robust financial future for your family? Understanding and proactively managing your Health Savings Account (HSA) in 2026 is more vital than ever, offering unparalleled tax advantages and a powerful tool for long-term financial health.

Understanding the 2026 HSA Landscape: New Limits and Eligibility

The year 2026 brings updated guidelines and contribution limits for Health Savings Accounts, making it essential for U.S. families to re-evaluate their strategies. These adjustments are designed to keep pace with rising healthcare costs and inflation, ensuring HSAs remain a highly effective savings vehicle. Eligibility for an HSA is tied to enrollment in a High Deductible Health Plan (HDHP), which typically features lower premiums but higher out-of-pocket costs before insurance coverage kicks in.

It is crucial to confirm that your health insurance plan qualifies as an HDHP for 2026. The IRS sets specific criteria for minimum deductibles and maximum out-of-pocket expenses that define an HDHP. Meeting these requirements is the first step toward unlocking the significant financial benefits an HSA offers.

Key HSA Eligibility Criteria for 2026

- Enrollment in a High Deductible Health Plan (HDHP).

- No other health coverage, with limited exceptions.

- Not enrolled in Medicare.

- Cannot be claimed as a dependent on someone else’s tax return.

The new contribution limits for 2026 represent an opportunity to save even more for future medical expenses, retirement, or unexpected health events. These limits are typically adjusted annually to reflect changes in the cost of living. Staying informed about these figures allows families to plan their contributions effectively, maximizing their tax-advantaged savings.

Understanding these foundational elements of HSA eligibility and the updated limits is the cornerstone of effective planning. By confirming your family’s eligibility and knowing the precise contribution thresholds, you lay the groundwork for a financially savvy approach to healthcare.

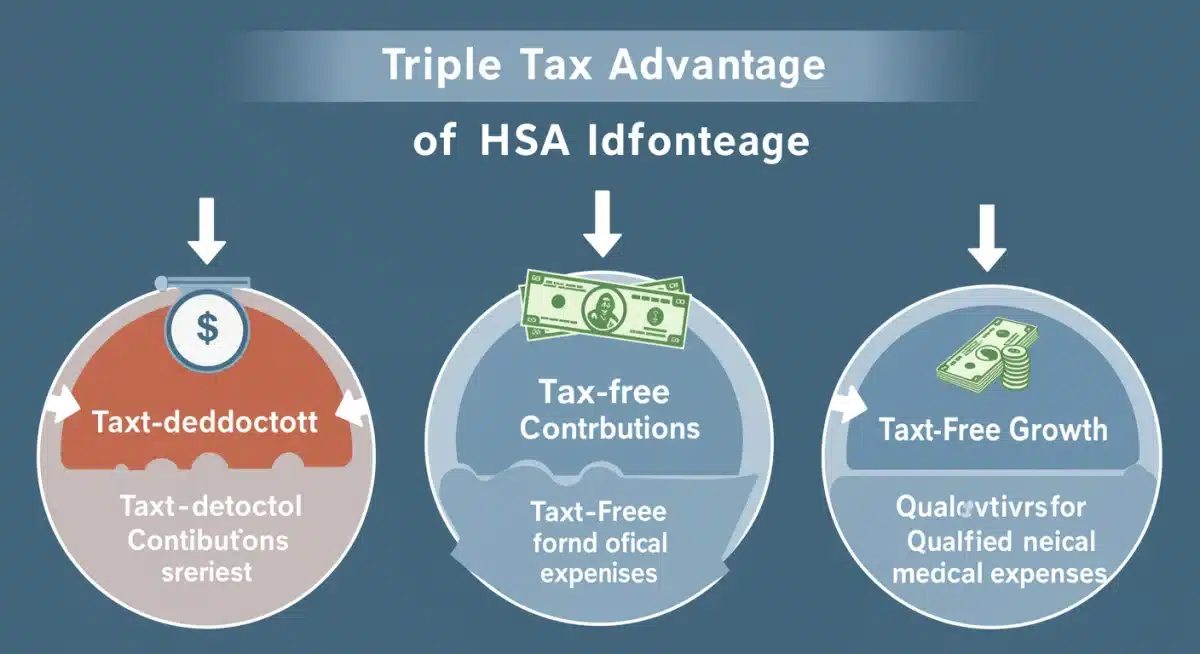

Unlocking the Triple Tax Advantage of HSAs

One of the most compelling reasons for U.S. families to prioritize HSA Maximization 2026 is the unparalleled triple tax advantage. This unique combination of tax benefits makes HSAs a powerful tool for both short-term healthcare expenses and long-term financial growth, rivaling even traditional retirement accounts.

The first advantage is that contributions to an HSA are tax-deductible. This means that any money you contribute to your HSA reduces your taxable income for the year, potentially lowering your overall tax liability. For many families, this immediate tax break can significantly impact their annual budget, freeing up funds for other priorities or further savings.

The second benefit is that your HSA funds grow tax-free. Unlike other investment accounts where earnings are taxed annually, any interest, dividends, or capital gains earned within your HSA are not subject to taxes. This allows your savings to compound more rapidly over time, accelerating your wealth accumulation, especially if you choose to invest your HSA funds.

Maximizing Tax-Free Growth

- Invest HSA funds in a diversified portfolio.

- Avoid early withdrawals for non-qualified expenses.

- Leverage compounding interest over decades.

Finally, qualified withdrawals from an HSA for eligible medical expenses are completely tax-free. This is arguably the most significant advantage, as it means you never pay taxes on the money you use for healthcare costs, from doctor’s visits and prescriptions to dental and vision care. This tax-free withdrawal feature extends into retirement, making the HSA a flexible and powerful savings vehicle for future medical needs.

The triple tax advantage transforms the HSA from a simple savings account into a dynamic financial instrument. By strategically contributing and investing, families can significantly reduce their tax burden while building a substantial nest egg dedicated to health-related expenditures, both now and in the future.

Strategic Contributions: Maximizing Your 2026 HSA Limits

To truly achieve HSA Maximization 2026, understanding and strategically utilizing the new contribution limits is paramount. The IRS typically adjusts these limits annually, and for 2026, families will have an increased opportunity to save. It’s not just about reaching the maximum; it’s about making consistent, informed contributions that align with your family’s financial goals and healthcare needs.

For individuals, the 2026 contribution limit will likely see an increase, and for families, this limit will be even higher. Additionally, individuals aged 55 and older are permitted to make an extra catch-up contribution, further boosting their savings potential. These limits are set by the IRS and are critical figures for your financial planning.

Contribution Strategies for Families

- Front-loading contributions: Contribute the maximum early in the year to allow more time for tax-free growth.

- Payroll deductions: Set up automatic contributions directly from your paycheck for convenience and consistency.

- Catch-up contributions: If eligible (age 55+), ensure you contribute the additional amount to maximize retirement healthcare savings.

Beyond simply contributing, consider how your contributions fit into your overall financial picture. If possible, aim to contribute the maximum allowed amount each year. This not only maximizes your tax deductions but also provides the largest possible pool of funds to grow tax-free over time. Even if you don’t use all the funds for immediate medical expenses, they roll over year after year, accumulating value.

Another smart strategy involves paying for current medical expenses out-of-pocket when feasible, and letting your HSA funds continue to grow. You can then reimburse yourself for those past qualified expenses years later, tax-free, once your HSA has accumulated significant value. This approach effectively turns your HSA into an additional investment account.

Strategic contributions are the bedrock of a high-performing HSA. By being aware of the 2026 limits, utilizing available catch-up provisions, and adopting smart contribution habits, U.S. families can significantly enhance their financial resilience against healthcare costs.

Investing Your HSA: A Path to Long-Term Wealth

Many individuals view their HSA solely as a savings account for immediate medical expenses. However, for those aiming for HSA Maximization 2026, understanding its potential as an investment vehicle is a game-changer. Once your HSA balance reaches a certain threshold, many providers allow you to invest the funds in various options, similar to a 401(k) or IRA.

Investing your HSA funds allows you to take full advantage of the tax-free growth component. Over decades, the power of compound interest can transform a modest HSA balance into a substantial sum, providing a significant financial cushion for future healthcare costs, especially in retirement. This long-term growth potential is often overlooked but is central to maximizing the HSA’s value.

Choosing the Right HSA Investment Strategy

- Assess your risk tolerance: Select investment options that align with your comfort level for risk.

- Diversify your portfolio: Spread your investments across different asset classes to mitigate risk.

- Consider long-term goals: Since HSA funds can be used in retirement, think about investment horizons spanning decades.

The types of investment options available through HSA providers can vary. They often include mutual funds, exchange-traded funds (ETFs), and sometimes individual stocks. It’s important to research your specific HSA provider’s investment platform, understand their fees, and choose options that are suitable for your financial goals and risk profile.

For those who are younger or have a longer time horizon until retirement, a more aggressive investment strategy might be appropriate, focusing on growth-oriented assets. As you approach retirement, you might consider shifting to more conservative investments to preserve your capital. The key is to actively manage your HSA investments, rather than letting the funds sit idly in a low-interest savings account.

By leveraging the investment capabilities of your HSA, you are not just saving for healthcare; you are building a tax-advantaged investment portfolio. This proactive approach to investing your HSA can lead to substantial wealth accumulation, providing greater financial security for your family’s health needs both now and far into the future.

Qualified Medical Expenses: What You Can Pay For Tax-Free

A critical aspect of HSA Maximization 2026 for U.S. families is a clear understanding of what constitutes a “qualified medical expense.” The ability to withdraw funds tax-free for these expenses is a cornerstone of the HSA’s appeal. Knowing the breadth of eligible expenses ensures you can confidently utilize your HSA without incurring penalties or unexpected tax liabilities.

The IRS provides extensive guidance on what qualifies, and it’s broader than many people realize. Beyond standard doctor’s visits, prescriptions, and hospital stays, HSAs can cover a wide array of healthcare-related costs. This includes dental care, vision care (including glasses and contacts), chiropractic services, psychological counseling, and even certain over-the-counter medications with a doctor’s prescription.

Examples of Qualified Medical Expenses

- Acupuncture and chiropractic services.

- Dental treatment, including braces and cleanings.

- Eye exams, glasses, contact lenses, and corrective surgery.

- Prescription medications and certain over-the-counter drugs.

- Therapy, including physical and occupational therapy.

It’s important to keep meticulous records of all your medical expenses, even those you pay out-of-pocket. This is because you can reimburse yourself from your HSA for any qualified expense incurred since your HSA was established, even if you paid for it years ago. This flexibility allows you to let your HSA funds grow through investment and then withdraw them tax-free later, a strategy known as the “HSA shoebox method.”

However, it’s equally important to understand what is not covered. Premiums for health insurance, with a few exceptions like long-term care insurance or COBRA, are generally not considered qualified medical expenses. Cosmetic procedures and general health items like vitamins (unless prescribed for a specific medical condition) are also typically excluded.

By thoroughly understanding the scope of qualified medical expenses, families can confidently budget and utilize their HSA to cover a significant portion of their healthcare costs, maximizing the tax-free withdrawal benefit and reinforcing their financial stability.

HSA as a Retirement Planning Tool for Families

While often viewed as a healthcare savings account, the HSA’s unique features position it as an incredibly powerful, yet frequently underutilized, retirement planning tool for U.S. families. For those committed to HSA Maximization 2026, integrating their HSA into their broader retirement strategy can yield significant long-term benefits, surpassing even traditional retirement accounts in some aspects.

After age 65, the rules for HSA withdrawals become more flexible. While funds can still be withdrawn tax-free for qualified medical expenses, they can also be withdrawn for any purpose without penalty, though these non-medical withdrawals will be taxed as ordinary income, similar to a traditional IRA or 401(k). This flexibility makes the HSA a versatile component of a retirement portfolio.

Integrating HSA into Retirement Planning

Using your HSA as a supplementary retirement account offers several advantages. First, the triple tax benefit continues into retirement, meaning your funds grow tax-free and can be withdrawn tax-free for medical expenses, which often increase in older age. Second, for non-medical withdrawals after 65, you avoid the 20% penalty that would apply if you made non-qualified withdrawals before age 65.

Many financial advisors recommend maximizing HSA contributions before contributing to other retirement accounts, especially if you anticipate significant healthcare costs in retirement. The tax advantages are simply too good to pass up. Unlike Flexible Spending Accounts (FSAs), HSA funds never expire and roll over year after year, making them ideal for long-term savings.

Consider the scenario where you have sufficient funds in your HSA to cover all your medical expenses in retirement. Any remaining funds can then be used for general living expenses, taxed at your ordinary income rate, providing an additional stream of income. This dual functionality — covering medical costs tax-free and acting as a flexible retirement income source — makes the HSA an indispensable asset.

By recognizing and leveraging the HSA’s potential as a powerful retirement planning tool, U.S. families can secure a more stable and financially comfortable future. It’s a strategic move that addresses both anticipated healthcare needs and broader financial independence in later life.

| Key Aspect | Brief Description |

|---|---|

| 2026 Limits | Updated contribution thresholds for individuals and families, crucial for maximizing annual savings. |

| Triple Tax Advantage | Tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. |

| Investment Potential | Opportunity to invest HSA funds for long-term, tax-free growth, enhancing retirement savings. |

| Retirement Tool | HSA funds can be used without penalty after age 65, making it a flexible retirement income source. |

Frequently Asked Questions About HSAs in 2026

To be eligible for an HSA in 2026, you must be enrolled in a High Deductible Health Plan (HDHP), have no other health coverage (with limited exceptions), not be enrolled in Medicare, and cannot be claimed as a dependent on someone else’s tax return. Meeting these criteria is fundamental.

The updated 2026 contribution limits for HSAs will likely be higher, allowing families to contribute more tax-deductible funds. This means greater tax savings on contributions and more money growing tax-free for future medical expenses or retirement, significantly boosting your financial health.

Yes, many HSA providers allow you to invest your funds once a certain balance is reached. The primary benefit is tax-free growth on your investments, which can lead to substantial wealth accumulation over time. This makes your HSA a powerful tool for long-term financial planning, beyond just immediate healthcare costs.

Qualified medical expenses are broad and include doctor’s visits, prescriptions, dental care, vision care, and even some over-the-counter medications. Keeping detailed records is crucial, as you can reimburse yourself for past qualified expenses, allowing your HSA funds to grow longer.

After age 65, HSA funds can be withdrawn for any purpose without penalty. While medical withdrawals remain tax-free, non-medical withdrawals are taxed as ordinary income, similar to a traditional IRA. This flexibility positions the HSA as an excellent supplementary retirement income stream, complementing other savings.

Conclusion

The Health Savings Account continues to stand as an indispensable financial instrument for U.S. families, especially with the anticipated 2026 updates to contribution limits and the enduring triple tax advantage. By understanding eligibility, strategically maximizing contributions, and leveraging the investment potential, families can transform their HSA from a simple savings account into a robust pillar of their financial and healthcare security. Proactive engagement with your HSA in 2026 is not merely about saving for medical bills; it’s about building long-term wealth, securing your retirement, and embracing a smarter approach to personal finance.

by $500 Annually")