2025 Guide: Maximize HSA Benefits, Save Over $700 Annually

The 2025 Guide to Maximizing HSA Benefits: Save Over $700 Annually on Healthcare Costs offers actionable strategies for optimizing your Health Savings Account, enabling substantial reductions in healthcare expenditures through strategic contributions and tax advantages.

Navigating healthcare costs can often feel like a complex puzzle, but with the right tools, you can transform it into a powerful savings opportunity. This comprehensive guide will show you how to effectively utilize and

maximize HSA benefits in 2025, potentially saving you over $700 annually on healthcare expenses and building a robust financial future.

Understanding the HSA Landscape in 2025

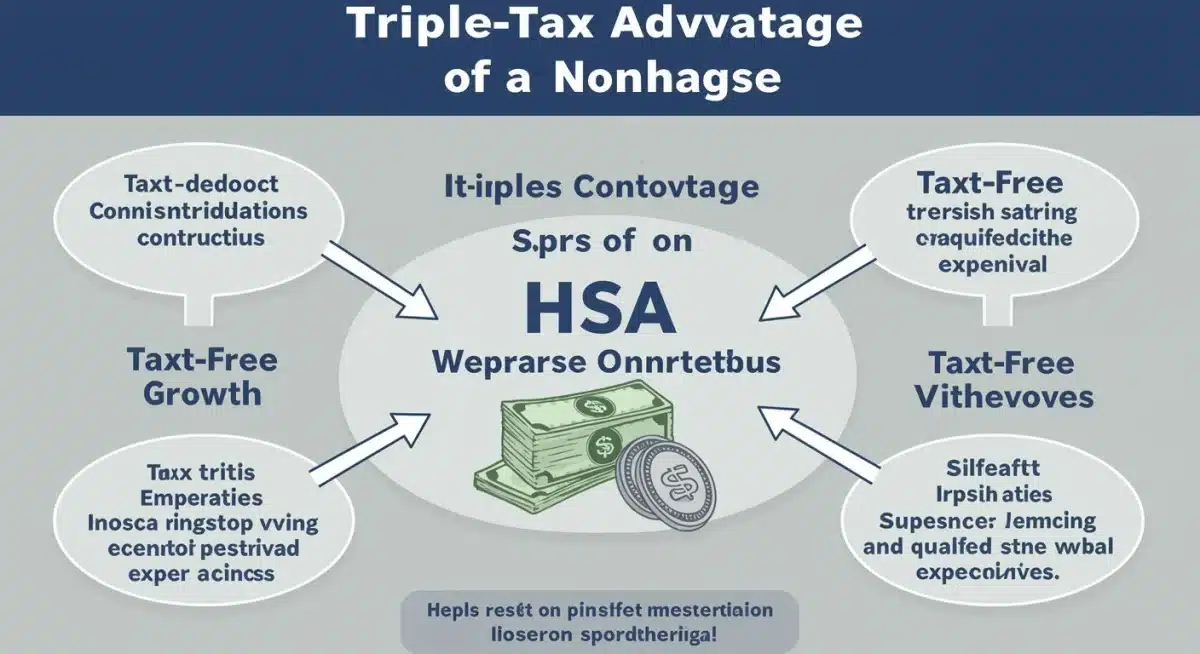

Health Savings Accounts (HSAs) remain an indispensable tool for Americans enrolled in high-deductible health plans (HDHPs). These accounts offer a unique triple tax advantage:

contributions are tax-deductible, earnings grow tax-free, and qualified withdrawals are tax-free. For 2025, understanding the updated contribution limits and eligibility criteria is crucial for anyone aiming to optimize their healthcare savings and financial planning.

The IRS typically adjusts HSA contribution limits annually, reflecting inflation and other economic factors. Staying informed about these changes is the first step towards maximizing your savings. These adjustments directly impact how much you can contribute

and, consequently, how much you can save in taxes and future medical costs. For individuals and families, these limits define the ceiling for their tax-advantaged savings, making it essential to plan contributions accordingly.

Eligibility requirements for an HSA

- Enrollment in a high-deductible health plan (HDHP) is mandatory.

- You must not be covered by any other health insurance that is not an HDHP (with some exceptions like dental or vision).

- You cannot be enrolled in Medicare.

- You cannot be claimed as a dependent on someone else’s tax return.

Meeting these criteria is fundamental. If you’re unsure about your plan’s HDHP status, consult your insurance provider or employer. Many individuals overlook these basic requirements, potentially missing out on significant tax advantages and long-term savings opportunities.

Ensuring eligibility is the gateway to unlocking the full power of an HSA, transforming routine medical expenses into a strategic financial asset. The ability to save for future medical needs while reducing current taxable income makes HSAs a standout option.

The landscape of healthcare finance is constantly evolving, and HSAs provide a stable and advantageous platform for managing health-related expenses. By understanding the foundational elements of HSA eligibility and contribution limits for 2025,

you lay the groundwork for a more secure financial future, ensuring you’re well-prepared for any medical eventuality while simultaneously building wealth.

Strategizing Your Contributions for Maximum Impact

Once you understand the eligibility and limits, the next step is to strategize your contributions. Maximizing your annual contributions is perhaps the most direct way to leverage HSA benefits. For 2025, ensure you are aware of the maximum contribution

amounts for both individual and family plans, including any catch-up contributions for those aged 55 and over. These limits represent the ceiling for your tax-advantaged savings and should be a primary target.

Many people only contribute enough to cover their expected medical expenses for the year. However, treating your HSA as a long-term investment vehicle can yield far greater returns. Unlike a Flexible Spending Account (FSA), HSA funds roll over year after year,

allowing for significant growth over time. This makes it an ideal complement to retirement planning, often referred to as a ‘triple tax advantage’ account.

Optimizing your contribution schedule

- Lump-sum contributions: If possible, contribute the maximum amount at the beginning of the year to allow for more time for investment growth.

- Payroll deductions: Set up automatic payroll deductions to ensure consistent contributions throughout the year, making it easier to reach the annual limit without feeling a significant financial strain.

- Catch-up contributions: Don’t forget the additional catch-up contribution for those aged 55 and older, which can significantly boost your savings potential.

Beyond just meeting the limits, consider how your contributions align with your overall financial goals. If you have the means, contributing the maximum amount each year can lead to substantial tax savings and investment growth. This strategy is particularly

effective for those who can afford to pay for current medical expenses out-of-pocket, allowing their HSA funds to grow untouched for decades. This approach positions the HSA as a powerful retirement savings tool rather than just a short-term healthcare fund.

Strategic contributions are the bedrock of a successful HSA strategy. By consistently contributing the maximum allowable amount, you not only reduce your taxable income but also build a substantial fund for future medical needs or even retirement.

This proactive approach ensures you are fully capitalizing on the unique financial advantages an HSA offers, transforming healthcare expenses into a vehicle for wealth accumulation.

Leveraging the Triple Tax Advantage

One of the most compelling aspects of a Health Savings Account is its triple tax advantage. Understanding and fully utilizing these benefits is key to maximizing your savings. First, contributions to an HSA are tax-deductible, reducing your taxable income

in the year you contribute. This immediate tax break can lead to significant savings, especially for those in higher tax brackets.

Second, the funds in your HSA grow tax-free. Many HSAs offer investment options similar to a 401(k) or IRA, allowing you to invest your contributions in stocks, bonds, and mutual funds. The interest, dividends, and capital gains earned within the HSA are not taxed,

allowing your money to compound more rapidly over time. This tax-free growth is a powerful engine for long-term wealth accumulation.

Understanding tax-free withdrawals for qualified medical expenses

The third and arguably most significant advantage comes with withdrawals. When you use HSA funds for qualified medical expenses, those withdrawals are entirely tax-free. This includes a wide range of expenses, from doctor visits and prescriptions to dental

and vision care. This tax-free withdrawal feature makes the HSA an incredibly efficient way to pay for healthcare throughout your life.

- Tax-deductible contributions: Reduce your current year’s taxable income, lowering your immediate tax burden.

- Tax-free growth: Your investments grow without being subject to capital gains or dividend taxes, accelerating wealth accumulation.

- Tax-free withdrawals: Funds used for qualified medical expenses are never taxed, providing significant savings on healthcare costs.

This combination of tax benefits makes the HSA a uniquely powerful financial tool. It’s not just a savings account for medical expenses; it’s a legitimate investment vehicle that can rival or even surpass other retirement accounts in terms of tax efficiency.

By strategically contributing, investing, and withdrawing, you can significantly reduce your overall tax liability and build a substantial nest egg for future healthcare needs or even general retirement expenses.

Embracing the triple tax advantage means recognizing the HSA’s potential beyond just a temporary holding place for medical funds. It becomes a cornerstone of a comprehensive financial strategy, offering unparalleled flexibility and tax efficiency.

This approach ensures that every dollar saved and invested within your HSA works harder for you, contributing to long-term financial security and peace of mind.

Smart Spending: Qualified Medical Expenses and Reimbursement Strategies

Knowing what constitutes a qualified medical expense is crucial for making tax-free withdrawals from your HSA. The IRS provides a comprehensive list, which includes everything from deductibles, co-payments, and prescription medications to dental treatment,

vision care, and even certain over-the-counter drugs. Understanding this list helps you avoid taxable withdrawals and maximizes the benefit of your HSA.

A common mistake is withdrawing HSA funds immediately to cover current medical costs. While this is certainly an option, a more strategic approach involves paying for current expenses out-of-pocket and saving your receipts. This allows your HSA funds

to continue growing tax-free, and you can reimburse yourself years, or even decades, later. This strategy transforms your HSA into an even more powerful investment vehicle.

The power of delayed reimbursement

By delaying reimbursement, you effectively create a tax-free investment account that you can tap into later in life. Imagine accumulating thousands of dollars in medical receipts over several years while your HSA grows. When you need a lump sum,

perhaps for retirement or a large medical expense, you can withdraw the accumulated amount tax-free by submitting your old receipts.

- Keep meticulous records: Save all receipts for qualified medical expenses, even if you pay out-of-pocket.

- Understand the IRS list: Familiarize yourself with what the IRS considers a qualified medical expense to ensure all reimbursements are legitimate.

- Consider future needs: Think long-term. Your HSA can be a significant asset in retirement when medical costs often increase.

This delayed reimbursement strategy is often overlooked but can be incredibly powerful. It allows you to maximize the investment growth potential of your HSA while still having the flexibility to access your funds tax-free for past medical expenses.

It’s like having a hidden, tax-free emergency fund or retirement account specifically for healthcare.

In essence, smart spending with an HSA isn’t just about paying for current costs; it’s about strategic financial planning. By understanding qualified expenses and employing delayed reimbursement, you turn your HSA into a dynamic tool for both immediate

and long-term financial well-being. This approach ensures you’re not just saving money, but actively growing your wealth while preparing for future healthcare needs.

Investing Your HSA for Long-Term Growth

Beyond simply saving, one of the most powerful aspects of an HSA is its potential for long-term investment growth. Many HSA providers offer investment options once your balance reaches a certain threshold, allowing you to invest your funds in a variety

of assets, similar to a 401(k) or IRA. This is where the tax-free growth truly shines, as your investments compound without being subject to annual taxes.

Choosing the right investment strategy for your HSA depends on your risk tolerance and time horizon. If you’re young and have many years until retirement, a more aggressive portfolio with a higher allocation to stocks might be appropriate. If you’re closer

to retirement, a more conservative approach with a mix of bonds and cash equivalents might be preferable. The key is to align your HSA investments with your broader financial goals.

Diversifying your HSA investments

Diversification is crucial in any investment portfolio, and your HSA is no exception. Spreading your investments across different asset classes and sectors can help mitigate risk and potentially enhance returns over time. Many HSA platforms offer a range

of mutual funds, exchange-traded funds (ETFs), and even individual stocks to choose from.

- Research investment options: Understand the fees and performance history of the funds offered by your HSA provider.

- Consider your time horizon: The longer your investment horizon, the more risk you can typically afford to take.

- Rebalance periodically: Review and adjust your portfolio annually to ensure it remains aligned with your risk tolerance and financial objectives.

Treating your HSA as a serious investment vehicle can significantly boost its value over time. The tax-free growth means that every dollar earned through investments is truly yours, without the drag of capital gains taxes. This can lead to a substantial

sum available for future medical expenses or, after age 65, for general retirement spending without penalty, though non-medical withdrawals will be taxed as ordinary income.

In conclusion, investing your HSA is not merely an option but a strategic imperative for long-term financial health. By actively managing your investments within the HSA, you transform it from a simple savings account into a powerful engine for wealth creation,

ensuring you’re well-prepared for both expected and unexpected healthcare costs down the line, all while enjoying unparalleled tax advantages.

HSA vs. FSA: Understanding the Key Differences

While both Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) are designed to help you save on healthcare costs, they operate under distinct rules and offer different benefits. Understanding these differences is crucial for choosing the

right account for your specific needs, especially when aiming to

maximize HSA benefits.

The most significant distinction lies in their rollover policies. HSA funds roll over year after year and are portable, meaning they stay with you even if you change employers or health plans. This makes HSAs excellent long-term savings and investment vehicles.

FSAs, on the other hand, typically have a “use-it-or-lose-it” rule, where most or all unused funds expire at the end of the plan year, though some plans allow a small rollover or a grace period.

Contribution limits and eligibility

Eligibility also differs considerably. HSAs require enrollment in a high-deductible health plan (HDHP), whereas FSAs are generally available to anyone whose employer offers one, regardless of their health plan type. Contribution limits also vary,

with HSAs often having higher limits, especially when factoring in catch-up contributions for those over 55.

- HSA portability: Funds belong to you and move with you, even if you change jobs.

- FSA rollover: Generally, funds expire at year-end, though some plans offer limited rollovers.

- HSA investment: HSAs can be invested, allowing for tax-free growth; FSAs typically cannot.

- Eligibility: HSA requires HDHP; FSA is employer-dependent.

Another key difference is the investment potential. HSAs can be invested, allowing your funds to grow tax-free over time, similar to a retirement account. FSAs are typically not investment accounts; they are solely for spending on current medical expenses.

This investment capability is a major reason why HSAs are often preferred for long-term financial planning.

In summary, if you are eligible for an HSA, it generally offers more flexibility, long-term growth potential, and tax advantages compared to an FSA, making it a superior choice for those looking to build substantial healthcare savings. However,

if you are not eligible for an HSA, an FSA can still be a valuable tool for reducing your taxable income and covering immediate medical expenses. Choosing between the two, or utilizing both if applicable, depends on your individual health coverage

and financial goals.

Integrating HSA into Your Overall Financial Plan

An HSA shouldn’t be viewed in isolation; it’s a powerful component of a holistic financial plan. By strategically integrating your HSA with other savings and investment vehicles, you can optimize your tax strategy, build wealth, and ensure financial security

for both immediate and long-term needs. Think of your HSA as a versatile tool that complements your 401(k), IRA, and other investment accounts.

One effective strategy is to prioritize maximizing your HSA contributions before fully funding other retirement accounts, especially if you anticipate significant healthcare costs in retirement. The triple tax advantage of an HSA often makes it a more

tax-efficient vehicle for healthcare savings than traditional retirement accounts, particularly when considering tax-free withdrawals for qualified medical expenses.

HSA as a retirement savings vehicle

For many, the HSA can serve as a supplemental retirement account. After age 65, you can withdraw HSA funds for any purpose without penalty, though non-medical withdrawals will be taxed as ordinary income. This flexibility makes it an attractive option for those

who have maxed out their other retirement contributions or are looking for an additional tax-advantaged savings vehicle.

- Prioritize contributions: Consider maxing out your HSA before other retirement accounts, especially if your employer doesn’t offer a 401(k) match.

- Complementary savings: Use your HSA to cover healthcare costs, freeing up funds in your 401(k) or IRA for other retirement expenses.

- Estate planning: HSAs can be passed on to beneficiaries, though specific rules apply depending on the relationship.

Another aspect of integration involves coordinating your HSA with your emergency fund. While an HSA is primarily for medical expenses, its liquidity and tax-free withdrawal for qualified costs can make it a secondary emergency fund. However, it’s generally

advisable to maintain a separate, easily accessible emergency fund for non-medical financial crises.

Ultimately, integrating your HSA into your broader financial plan means recognizing its unique advantages and positioning it to work in harmony with your other financial tools. This comprehensive approach ensures that you’re not only prepared for healthcare

expenses but are also optimizing your tax situation, growing your wealth, and building a resilient financial future for yourself and your family. The goal is to create a seamless financial ecosystem where each component reinforces the others.

| Key Aspect | Brief Description |

|---|---|

| Triple Tax Advantage | Contributions are tax-deductible, earnings grow tax-free, and qualified withdrawals are tax-free. |

| Contribution Limits 2025 | Stay updated on annual IRS adjustments for individual and family maximum contributions. |

| Strategic Investing | Invest HSA funds for long-term, tax-free growth, aligning with your risk tolerance. |

| Delayed Reimbursement | Pay out-of-pocket for current expenses, save receipts, and reimburse tax-free later. |

Frequently Asked Questions About HSAs in 2025

The IRS typically announces new limits in late fall of the preceding year. While specific 2025 numbers are pending, they are expected to increase slightly from 2024 due to inflation. Always check the official IRS website or with your HSA administrator for the most current figures to ensure maximum contributions.

You can, but it’s generally not recommended before age 65. Withdrawals for non-medical expenses before age 65 are subject to your ordinary income tax rate plus a 20% penalty. After age 65, non-medical withdrawals are taxed as ordinary income but without the penalty, acting like a traditional IRA.

An HSA can be a powerful complement to a 401(k). While a 401(k) match should always be prioritized, an HSA’s triple tax advantage (deductible contributions, tax-free growth, tax-free withdrawals for medical) makes it an excellent choice for healthcare expenses in retirement, sometimes even more tax-efficient than a 401(k) for that specific purpose.

Your HSA is portable, meaning it belongs to you, not your employer. If you change jobs, you can keep your existing HSA and continue to contribute to it, provided you remain enrolled in an HDHP. You can also roll it over to a new HSA provider if you prefer.

Generally, no, not a full-purpose FSA. You cannot contribute to both a regular HSA and a regular FSA in the same year. However, you might be able to have an HSA alongside a Limited Purpose FSA (LPFSA) which covers only dental and vision expenses, or a Post-Deductible FSA, which activates after your HDHP deductible is met.

Conclusion

The 2025 Guide to Maximizing HSA Benefits: Save Over $700 Annually on Healthcare Costs underscores the immense potential of Health Savings Accounts as a cornerstone of smart financial planning. By understanding eligibility, optimizing contributions,

leveraging the triple tax advantage, and employing strategic spending and investment practices, individuals and families can significantly reduce their healthcare burden while simultaneously building substantial long-term wealth. Integrating your HSA into your

overall financial strategy ensures not just preparedness for medical expenses but also a robust pathway to financial independence. Proactive management of your HSA is key to unlocking these profound benefits and securing your financial future.

by $500 Annually")

2026: New Limits & Investment Strategies")